ALERT: It is important to understand all legal and financial consequences of a short sale before listing your property as such, as every situation is different. Be sure to discuss your scenario with your accountant or financial adviser, tax attorney and an experienced short sale real estate agent.

************

What is a short sale?

A short sale is when your lender agrees to sell your home for less than what is owed on the mortgage. In order to short sale your home your lender must agree in writing to the sale. Typically this is done once you present an offer from a buyer to the lender, but there are some lenders that have programs to pre-approve your short sale before you list your property.

Why would a bank choose to accept a short sale?

Because foreclosures are very expensive (they usually cost the lender about $20,000, plus often times the lender has to make repairs on the home prior to resale). The lender can save potentially hundreds of thousands of dollars in legal fees, maintenance fees, property taxes and upkeep.

Can I get money for short selling my home?

There are programs out there, both government-run (federal and state) and lender-run, that will allow you to get paid at the close of escrow. Payments can run from several thousand dollars to tens of thousands of dollars. You need to look into these programs and see if you qualify. For more information on some of the different programs check with your lender, your state and your Realtor. See below for more information.

Why should you consider a short sale?

-There will be less of an impact to your credit score than with a foreclosure -Ability to buy a home in a shorter time down the road

Short sale process: The short sale begins with finding a Realtor who has extensive knowledge of the short sale process. At that point the agent will take the following steps: 1. Collect all necessary financial information. Your agent will evaluate what your lender(s) needs in order to get the process started, including providing you with lender forms for you to fill out that need to be sent to the lenders. 2. Negotiate with any subsequent (second) lenders. 3. Market analysis/pricing. Your agent will prepare a complete market analysis and list your property (some lenders will dictate what the price needs to be if you are going through a short sale pre-approval program, otherwise your agent will discuss value with you). 4. Marketing. Your agent will market your home just like a regular sale, counsel you on how to make your property show it’s best, and discuss showings with you. Keep in mind that although you are selling your home via a short sale, you still want to make sure it is in the best showing condition possible. 5. Offers. Once an offer is presented and accepted by you, your agent will submit it to the bank, along with other documentation, in order for approval. 6. Approval. Upon approval of the bank, escrow will be opened and the buyers will proceed with their due diligence. This is the part of the short sale that can take a long time, depending on the lender(s). 6. Deadline. Lenders give a deadline by which escrow must close. If it is not closed by this time the short sale will not go through and an auction date will be set/followed through. It is possible to get extensions from some lenders in some situations.

***

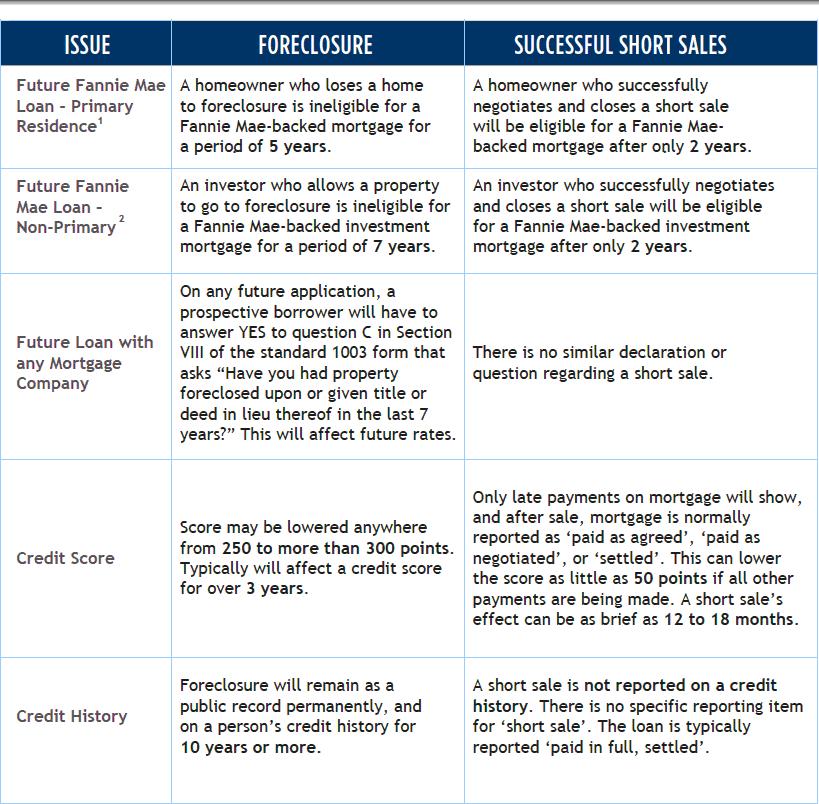

How is my credit affected? When can I repurchase? A short sale will show up on your credit report as a discharged debt, for less than the amount owed. This will affect your credit score, but not as much as with a foreclosure. Usually you will be able to repurchase within 2-3 years.

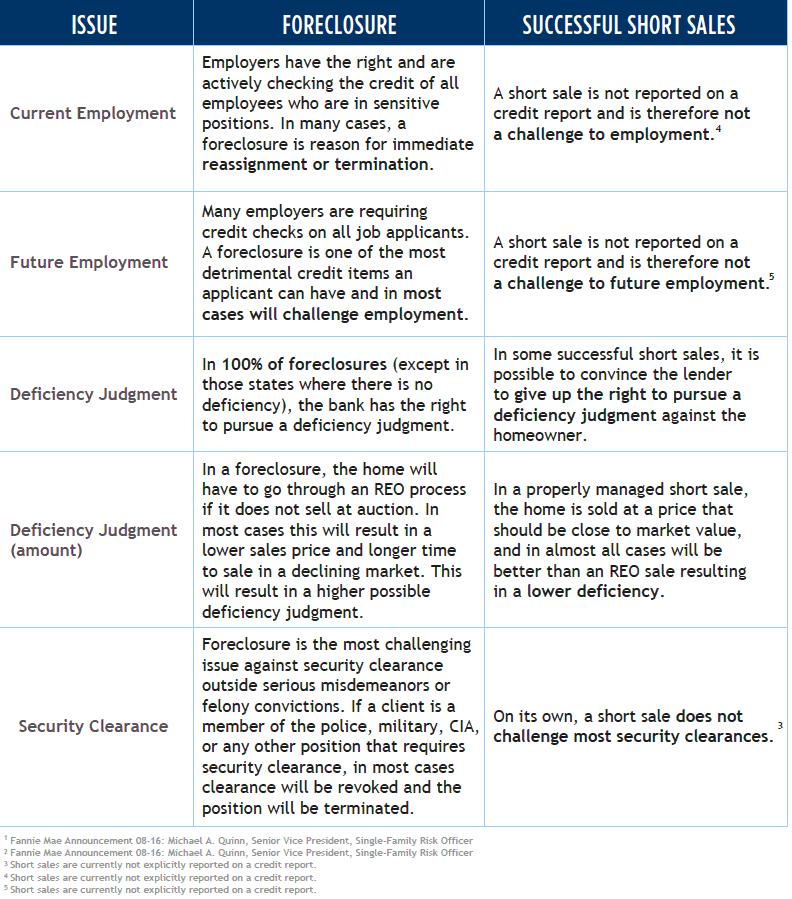

With a foreclosure, your credit score will be hit much harder, as it will show that you were unable to fulfill a financial responsibility. This can result in the inability to repurchase for possibly 7 years or longer. Consult with your financial adviser before deciding whether to short sale.

***

Tax Ramifications Under the Mortgage Forgiveness Debt Relief Act of 2007*, with a short sale a borrower was not liable for taxes on the capital gain (the difference between what you sold the property for and what you owed). However, as of January 1, 2014 this act expired and has not yet been retroactively extended. In some states, like California, a lender is not allowed to pursue you legally if it approves a short sale. Consult with your accountant or financial adviser to see how your taxes may be affected before deciding to short sell your home.

*The Mortgage Forgiveness Debt Relief Act requirements: it only applies to your principal residence (cannot be investment property or a 2nd home), and only to the original purchase price, plus improvements on your principal residence; there is a limit to the debt to be forgiven – of $2,000,000; there may be a possibility of taxation at a later date – discuss with your accountant.

IMPORTANT: Any short sale that closes after the January 2014 expiration date could subject you to taxation on the difference between the sales price and what you owe (e.g. if you owe $300,000 and sell your home via a bank-approved short sale for $250,000, you could be taxed on the $50,000 difference. Based on a marginal tax rate of 36%, you could owe $18,000 in taxes).

HOWEVER, under California law, those who short sale their primary residence are allegedly assured under the CA Code of Civil Procedure that no federal tax penalties will be incurred even though the Act has expired. The anti-deficiency provision is part of the CA Code of Civil Procedure, section 580e, and labels the debt as a “non-recourse obligation” – for federal income tax purposes the homeowner will be considered to have no COD income. Furthermore, the California Franchise Tax Board also claims that distressed California homeowners are protected against any state income tax from a short sale once the sale of the home is completed. For more information and details about exemptions, it is important to contact your tax professional and/or the state of California.

***

What is a deed in lieu of foreclosure, and how is it different from a short sale? A deed in lieu of foreclosure is when the borrower gives the property deed to the lender, conveying all of his/her interest in the real property to the lender in order to satisfy the loan that is in default. Both the borrower and the lender must enter into the transaction voluntarily – the lender has no obligation to accept the deed. This differs from a short sale because there is no sale of the property to a third party – the lender simply takes the deed. There are certain requirements that must be met, as well as some restrictions (i.e. it does not apply to FHA loans), and the agreement must be in writing. There are possible tax and definitely some credit ramifications, so speak with your financial adviser before choosing a deed in lieu.

Programs to Help You/Financial Incentives Upon Completion of Successful Short Sale There are several programs out there that offer financial incentives to homeowners who qualify for and complete a successful short sale. Here are some of those programs, but you are advised to consult with your lender and your real estate agent to see which programs may be available to you.

- HAFA.

- Transition Assistance Program (TAP).

- Bank of America Cooperative Short Sale Program.

- Chase and Citi Short Sale Programs.

- Other bank programs

The Home Affordable Foreclosure Alternatives program (HAFA) gives qualified sellers up to $3000 at closing. This program applies to both short sales and deeds in lieu of foreclosure. There are requirements to qualify, so discuss with your Realtor. For more information visit http://www.makinghomeaffordable.gov/programs/exit-gracefully/Pages/hafa.aspx

This is a California program, which is part of Keep Your Home California, that nets qualified state homeowners up to $5000 at completion of a short sale or deed in lieu of foreclosure. To check eligibility and get further information, visit http://keepyourhomecalifornia.org/tap.htm to check eligibility and get information.

This program is available to any B of A loan holders who are doing a short sale, and provides up to $2500 to those who qualify. The difference between this program and HAFA is that B of A preapproves the home for short sale, including the list price (which could be an issue). A 4 month time frame is given in which the agent must sell the home, and at the end of that time if the home has not sold B of A will issue an automatic deed in lieu of foreclosure (which could be a problem). Speak with your agent if you are not sure about how this program compares to HAFA, as the market time restrictions could be an issue. If you have a loan with B of A, contact them to get more information on the program.

Both of these lenders have initiated aggressive programs that pay up to $20,000-35,000. But don’t get too excited just yet…in order to partake of this program you need to receive a letter from one of these banks. This program is not owner-initiated. The banks find those homeowners whom they feel meet standards to successfully qualify.

Some other banks are jumping on the bandwagon and offering their own short sale versions. Some banks send letters to sellers asking them to participate in short sales, with a financial incentive at closing (between $3000-5000). Other banks have their own programs and more are sure to follow.

Many lenders are creating their own programs to bypass the HAFA program, as it limits the ability of the banks to collect money. With their own programs, controlling many of the terms of the short sale (like price and time frames), they stand to gain a lot more. But if you are going to use any bank programs you need to research and understand them, so that you are able to make an informed decision as to which one to choose. As always, knowledge is power.

** It is important to note that there were a few lenders that offered programs to their borrowers that paid big bucks to short sale sellers. Both Bank of America and Chase, for example, have been known in the past to award up to $30,000 to homeowners upon completion of successful short sales. If you are considering a short sale, make sure you discuss with your agent/negotiator potential programs that may be available to you. For example, some banks require that the lender reach out to you, and you cannot opt into the programs. Every program is different, so make sure to obtain the information BEFORE you list your home.

Are there other options to a short sale? There very well may be. We advise you to consult with your accountant, attorney, lender, and a skilled Realtor so that you can understand what other possible options may be available to you. Some possibilities include loan modification, postponement, strategic default, military options, foreclosure, and bankruptcy. You need to understand which one is right for you and your loved ones before agreeing to any single method.

HARP2: Avoiding Foreclosure and Short Sale The Home Affordable Refinance Program is entering it second phase, which may provide further options to homeowners that will allow them to stay in their homes and avoid foreclosure. If you are not in default on your loan and owe more than the current market value of your home, you may qualify for a refinance under HARP.

The new rules allow qualified homeowners to refinance up to the amount of the outstanding loan on a principal residence, including any amount in excess of 100% of the value (the old HARP restricted that to 125% of current market value).

Here are the requirements:

- Loans must be current, with a good 12 month payment history (no late payments in the last 6 months, only one allowed in the last 12 months)

- Loan must be financed by either Fannie Mae or Freddie Mac, or must have been purchased by either before May 31, 2009.

- No appraisals or underwriting will be required (but there may be an inspection of the home)

- The mortgage can not have previously been refinanced under HARP

Contact your lender and discuss with your CPA/financial planner to determine whether HARP is right for you, keeping in mind that HARP is not a principal reduction, and refinancing a loan on a home that is worth less than the loan is something you need to feel comfortable about. If you would like further information on the HARP program, click here.

Rachel LaMar, ©2011-2017

If you have any questions about short sales that are not answered here, please send an email to Rachel(at)LaMarRealEstate(dotted)org, and it will be added to this page

Short Sale vs. Foreclosure

©2026